Every November, we host an annual meeting for all of our investors (limited partners) in the various Precursor Ventures funds. We typically don’t share any of the content we present outside of that group, but I decided to share a few slides to give folks a glimpse into some of the things we are seeing in the pre-seed and seed ecosystem.

In the past few years, quite a bit has changed in the pre-seed and seed investing landscape. Before I get into the data, I want to clarify a few things:

- We have a strict internal definition for pre-seed rounds. For our purposes, a pre-seed round is a round of $1 million or less for a company that is likely pre-launch and pre-traction. We are strict on the round size and a bit more flexible on the other conditions. Anything that does not meet that criteria is classified as a seed-stage investment for our internal purposes.

- We don’t see every company in the market (obviously) – this data reflects what we know from the companies we have actually invested in and worked with since starting Precursor.

- This data reflects companies that have successfully raised large milestone Series A rounds. We have a very large portion of the portfolio that did not raise this year and I suspect the data will change a bit when we see what happens for the companies that raise Series A rounds in 2023 and 2024.

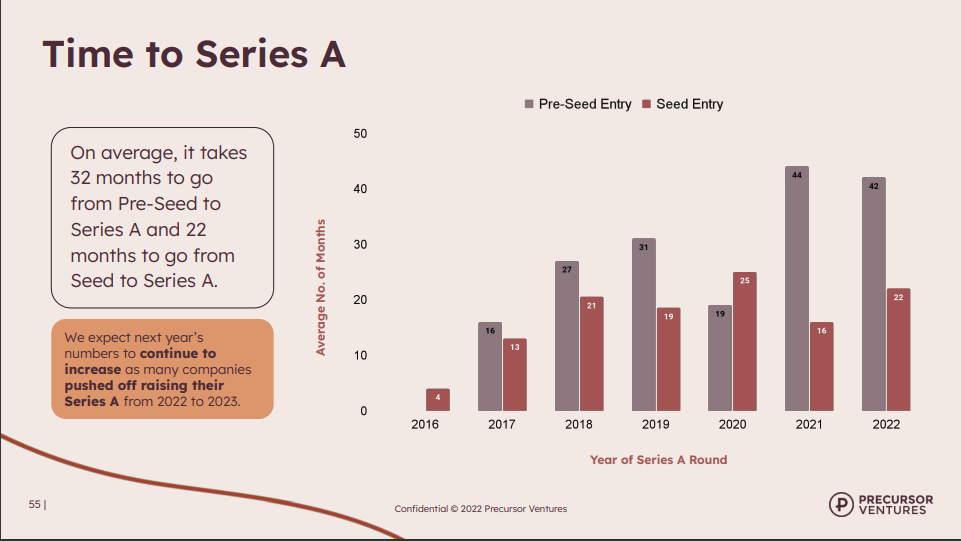

The Time from Pre-Seed to Series A is Getting Longer

One thing that is certainly true is that the time required to get to Series A from the pre-seed has gotten longer over time. We also do some seed investing – we will enter at seed for companies that raise more than $1 million to get started, and some are companies that had friends and family rounds or pre-seed rounds where we did not participate. I am showing the seed data next to the pre-seed data for comparison purposes.

The time required to get from pre-seed (by our definition) to Series A has gotten longer over time. There are many reasons that this is the case, including a higher bar for Series A graduation, our decision to continue to back companies that need 1-2 years to find product market fit and start to scale, and the current fundraising environment.

It Takes More Money to Get to Series A from Pre-Seed Over Time

It should come as no surprise that the amount of money required to get to a Series A round over time has increased; as the chart above noted, the time required has increased and time and money are highly correlated for most startups.

I have one caveat for this chart. Instead of looking at Series A vintage year, we looked at this data by fund. The fact that the amount of capital required for the Fund III cohort is lower reflects the fact that fewer of those companies have graduated to Series A relative to our previous funds. With maturity, I expect the Fund III cohort to show a continued increase in the amount of capital required to get to a Series A round from the pre-seed starting point. We just don’t have all of that data yet.

It Takes More Rounds of Capital to Get to a Series A

If you’ve read this far, it won’t come as any surprise to you that it takes more discrete rounds of financing for our pre-seed companies to get to Series A. Identifying what constitutes a discrete round is tricky in a world where companies can raise on SAFEs whenever the timing is right. We try to delineate rounds based on the terms and timing of the raise. It’s not an exact science, but I think the way we account for discrete rounds largely maps to the way that our portfolio company founders think about and execute their own fundraises.

The multiple rounds of capital required to get to Series A from pre-seed creates a host of challenges. What do you call each of these subsequent rounds? How do founders manage dilution across multiple rounds of pre-seed and seed financing prior to a Series A round? Which set of investors should get diluted if founder ownership drops below acceptable thresholds? How do you even forecast founder ownership in a world where a company has 3 SAFEs that have yet to convert prior to a Series A round? In many ways, the number of financings required to get to a Series A creates more complexities and challenges than the amount of capital that needs to be raised or the time required. Maybe I will write more about that some time in the future – it’s a meaty topic.

I am sharing this data because all of this information informs how we at Precursor think about how to price rounds, how much money to set aside for follow-on financings, how we think about capital needs for the companies we back, and how we advise founders on their own fundraising journeys. I know that other pre-seed investors likely have data that looks different and I am sharing what we have seen in the interest of sharing one perspective. I hope this helps founders think through the many paths they may encounter as they seek to scale their businesses.

This is great to think about. Thanks for sharing